Destination 2050 Roadmap

How can aviation reach net zero? Whilst a large and complex question, the recently released Destination 2050 Roadmap seeks to provide not only an answer, but a clear pathway to reach it. In this month’s Five Minute Feature, we sit down with Elisabeth van der Sman from Royal Netherlands Aerospace Centre (NLR) – one of the NLR/SEO developers of the roadmap – to dive into exactly how the roadmap was developed from a scientific perspective.

Elisabeth van der Sman is senior consultant and team leader for sustainable aviation at Royal NLR. Amongst other things, she specialises in research on the impact of Sustainable Aviation Fuels (SAF) and new energy carriers, such as hydrogen, on sustainable aviation. She is passionate about making sure that dialogues and discussions are conducted with a sound scientific basis – ‘this role lets me play a tangible part in making aviation more sustainable,’ she notes. ‘That feels good.’

The updated Destination 2050 Roadmap is a loud wake-up call, particularly for policymakers. From a scientific perspective, why is immediate action so critical?

The short answer is that things take time. If you want to have a significant impact on CO2 emissions by 2050, the work must begin now in order for that effective scale to be in place by 2050. Reducing CO2 emissions in the long term requires action now to begin a cumulative effect.

You can see this, for example, when it comes to hydrogen. In the updated Roadmap, entry into service of a hydrogen-powered single-aisle is 5 years later than in the initial Roadmap. Although the estimated market penetration is also reduced, this 5 year delay is a key factor of the reduced contribution from hydrogen in this updated roadmap.

The need for quick action and rapid scale-up also holds for renewable energy deployment, and in particular, Sustainable Aviation Fuels (SAF). If we want to reach 80% SAF usage by 2050 – 10% higher than the ReFuelEU Aviation Regulation’s SAF target of 70% – we must ensure the production capacity, infrastructure and investments are in place now, so that we can meet the physical demand for SAF. We simply must start now – this makes our short-term decisions critical for ensuring we have a net-zero future.

The new roadmap reaffirms the technological, logistical and policy challenges hindering European aviation’s decarbonisation efforts – really spelling out its hard-to-abate nature. We now know that the sector’s net zero pathway is on a 1.7C Celsius trajectory rather than 1.5C. Could you explain what does it mean in concrete terms?

Aviation is a hard-to-abate transport sector. As I said previously, actions to reduce emissions take a significant amount of time to scale up and become effective. Additional measures and substantial investments would be required to be compatible with carbon budgets that are in line with keeping long-term global warming to 1.5°C pathway with a 50% likelihood. The feasibility, impact and implications of additional measures have not been analysed in the report.

However, the Roadmap does outline several concrete measures that can ensure we can reach the 1.7C target, if they are introduced immediately. This includes:

| Pillars | Short-term actions for meeting the roadmap pathway |

| Aircraft and engine technology | Ensure that aircraft not yet introduced enter into service as plannedMitigate any possible funding gaps to prevent delays in R&D |

| ATM and operations | Timely implementation of ATM Master Plan objectivesImplement SESAR solutions and enabling technologies more quickly |

| Alternative fuels | Support for supply chain development, increased feedstock availability and renewable energy deployment to increase SAF uptakeDevelop a financial support system for investments in production facilities |

| Economic measures | Establish a net zero target for all market-based measuresIncrease quality/effectiveness of carbon offsets within CORSIASet policy for high-quality carbon removals within the EU Emissions Trading System (EU ETS) |

To analyse compatibility with temperature targets, the Destination 2050 partners tasked you to model aviation’s remaining carbon budget. What were the key components of this modelling?

The modelling consists of two distinct parts. Firstly, the Destination 2050 Roadmap has, for the first time, calculated the total – cumulative – emissions of European aviation for the period up to and including 2050. Secondly, this was compared to a carbon budget for European aviation. The first part – calculating the total emissions between 2020 and 2050 – is more straightforward. The second – determining the carbon budget for European aviation – is much more complex.

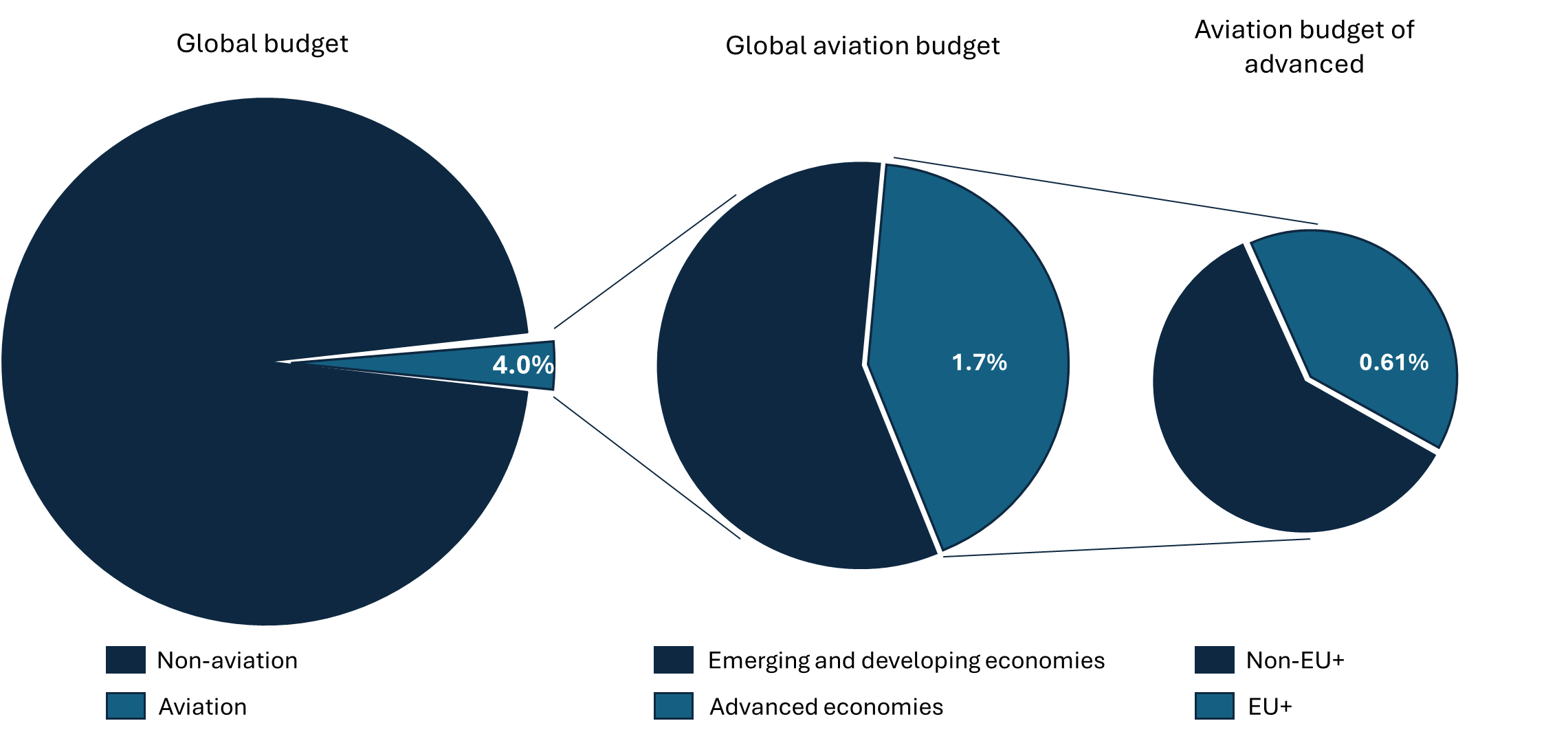

We began by determining what percentage of a global carbon budget would be available for global aviation, and what percentage of that would, in turn, be available specifically for European aviation. This entire process can be seen in the graph below. We used the IEA Net Zero Roadmap’s estimate that aviation accounts for 4.0% of global emissions between 2020 and 2050. The European share was further refined by analysing the proportion of aviation emissions within advanced economies, leading to a 0.61% allocation for EU+ aviation. This percentage was applied to two global carbon budget scenarios – 400 GtCO₂ (for a 50% chance of limiting warming to 1.5°C) and 600 GtCO₂ (for a 66% chance of limiting warming to 1.7°C) – resulting in carbon budgets of 2.46 GtCO₂ and 3.68 GtCO₂, respectively.

With projected aviation emissions for 2020 to 2050 totalling 3.30 GtCO₂, the roadmap aligns with the 1.7°C target but exceeds the budget required to limit warming to 1.5°C.

What are the main reasons behind the increased costs of decarbonisation for aviation vs the previous estimates published in The Price of Net Zero report?

To achieve net zero CO2 emissions, additional efforts and therefore additional costs are required. These additional costs are in the magnitude of €1,300 bn over the course of the next 25 years. The primary cause is the increasing cost estimates for SAF. Previously, we have used the production costs of SAF to build estimates. In this Roadmap, we have used estimated market prices for SAF – that include a mark-up for producers and others in the supply chain- based on the newest available literature on SAF costs. This is significant: we previously estimated a cost premium with respect to conventional kerosene of €440 billion. This figure has grown to €765 billion.

Additionally, there are smaller increases across other pillars and measures. Technology R&D costs have slightly increased due to a larger variety of future aircraft, fleet renewal costs have gone up due to an increase in fleet size. On the other hand, the required investments related to the infrastructure needed for alternatively fuelled aircraft have reduced due to a lower share of hydrogen-powered types within the fleet. Finally, Air Traffic Management (ATM) and operational expenditures have slightly reduced, whereas costs for economic measures have increased (from just over €152 billion to €220 billion).

Sustainable Aviation Fuel (SAF) emerges as the CO2-slashing hero in this roadmap, with the roadmap aiming for SAF to be 80% of used fuels by 2050. The use of SAF and the related demand impacts could reduce emissions by 55% alone. What particular challenges need to be overcome to realise its decarbonisation potential, and who holds the greatest influence over its development and deployment?

This 80% share of SAF – 10% higher than the ReFuelEU Aviation Regulation – is an ambitious goal. As mentioned previously, scaling up facilities and meeting such larger demand will take time and we simply must act now to ensure we meet this goal in the future. Several challenges need to be tacked to realise this:

- Deployment of renewable energy to produce the required amount of electricity for hydrogen production – for sure as a fuel and as a building block for synthetic SAF,

- Mobilisation and development of biomass supply chains to produce non-synthetic SAF,

- Funding is essential – both private and public – to ensure SAF production facilities can meet demand,

- Bridging the price gap between SAF and conventional aviation fuel to ensure additional uptake,

- Ensuring that aircraft are ready for SAF blends above its current regulatory maximum blend rate of 50%: research is promising in this respect.

With the updated roadmap in hand, what are the biggest unknowns on the science front that could shape the industry’s path to net-zero?

I would like to be clear: the biggest uncertainties and challenges are not scientific. They relate to policy, investments, market dynamics and the timely implementation of the measures required to follow the Destination 2050 roadmap pathway.

The next few years will be crucial – and as such, our top priority should be the implementation and monitoring of the roadmap to ensure we can meet our decarbonisation goals.

This roadmap report, commissioned by the Destination 2050 partners and developed by Royal NLR and SEO Amsterdam Economics, provides an update on the pathway to net-zero European aviation, first published in 2021.

At both international and European levels, progress has been made to decarbonise the sector, demonstrating the commitment of both industry and governments to this critical objective – all while ensuring Europe maintains its leadership in sustainable aviation innovation and competitiveness. Now, more than ever, time is of the essence for policymakers to work shoulder-to-shoulder with the aviation sector to make this happen. The industry is calling on regulators to develop supporting policies, including:

- Aviation being recognised as a hard-to-abate, strategic sector for Europe and as such to be included in the new legislative attempts to revive industrial competitiveness in the EU (i.e. Clean Industrial Deal),

- As part of such inclusion, that a dedicated Aviation Industrial Strategy be developed with specific focus on the scale up and uptake of affordable Sustainable Aviation Fuels,

- Accelerate innovation, support research and foster funding for aviation decarbonisation.

With this in mind, the Destination 2050 partners lay out several concrete policy recommendations and the report shows a clear and actionable pathway to achieve net-zero aviation emissions by 2050.

Find the full roadmap here: https://www.destination2050.eu/roadmap/

Destination 2050 Partners:

ACI EUROPE

Airlines For Europe (A4E)

Aerospace, Security and Defence Industries Association of Europe (ASD)

Civil Air Navigation Services Organisation (CANSO)

European Regions Airline Association (ERA)